Why should you invest in a 401(k)? One might think the only reason is to take advantage of tax advantage growth, but there are many other reasons for investing in a 401(k).

Tax-Advantaged Growth

Investing in a workforce 401(k) plan offers the primary advantage that the funds will grow with some form of tax benefit—whether that is through traditional or Roth contributions. In a traditional 401(k), contributions reduce current taxable income, allowing more money to be invested upfront while delaying taxes until retirement. A Roth 401(k) is funded with after-tax dollars, but both the original contributions and any investment earnings can be withdrawn tax-free if certain conditions are met. This distinction allows individuals to choose whether it is more beneficial to receive a tax break now or in the future, depending on their expected tax situation [1]. More detail on the differences of traditional vs. Roth contributions can be found here.

Immediate Tax Savings for Traditional 401(k)s

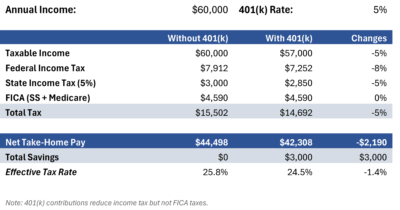

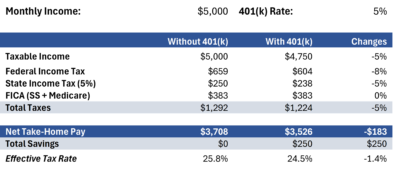

Contributions to a traditional 401(k) create immediate tax savings as income taxed at the marginal tax rate is reduced by the amount of the contribution leading to a lower average tax rate. For example, if you make $60,000 annually ($5,000 monthly) and you contribute 5% of your monthly pre-tax income, your paycheck would be reduced by $250 each month or $3,000 annually. However, due to the tax deferral your net pay would only be reduced by $183 or $2,190, assuming a 22% marginal and 5% state tax rate (see Appendix).

Protection from Creditors

Assets within 401(k) accounts are protected from commercial creditors under the Employee Retirement Income Security Act (ERISA), making them safeguarded in bankruptcy proceedings and against liability payments resulting from lawsuits [2][3]. Retirement savings inside a 401(k) plan remain secure during times of financial hardship or distress, providing a reliable safety net for retirement years.

Automatic Savings

Contributing to a 401(k) helps establish disciplined savings habits for retirement by placing funds in an account that is intentionally designed to be difficult to access before retirement age [4]. This encourages long-term savings, as early withdrawals often come with penalties and tax consequences, making it unfavorable to withdraw assets before retirement. This leads individuals to be more likely to maintain retirement savings that support their standard of living, while also reinforcing the value of delayed gratification, a key principle when saving for long-term goals. Often the employer matches a certain percentage of your 401(k) contribution. More on matching can be found here.

Other Considerations

To avoid having to withdraw funds early it is essential to build an emergency fund that covers 3–6 months of non-discretionary expenses [5]. This financial cushion helps protect retirement savings from being used for short-term needs, allowing the 401(k) investments to grow uninterrupted and fulfill their long-term purpose.

Appendix

Exhibit A: Annual 401(k) Contribution Tax Impact

Exhibit B: Monthly 401(k) Contribution Tax Impact

Disclaimer

This commentary is intended solely for informational and educational purposes and does not constitute legal, tax, investment, or accounting advice. It does not represent an offer to sell or a solicitation of an offer to buy any security, financial instrument, or investment interest. Any such offer or solicitation will be made only through formal offering documents and in accordance with applicable laws and regulations.

Certain statements contained herein may include forward-looking information, hypothetical illustrations, or projections. These are based on current assumptions and expectations, which are subject to change and involve known and unknown risks and uncertainties. Actual outcomes may differ materially due to factors such as financing availability, regulatory approvals, market volatility, force majeure events, competitive pressures, and other unforeseen circumstances.

No representation or warranty is made regarding the accuracy, completeness, or reliability of the information presented. Past performance is not indicative of future results.

This material may reference potential interest rate or market trends that are not guaranteed and may differ materially from actual results. The information herein should not be relied upon as a guarantee or forecast of future performance or interest rate movements.

This document is proprietary and may not be reproduced, distributed, or shared without prior written consent. By accepting this commentary, the recipient agrees to use it solely for its intended purpose.

Porter White & Company (“PW&Co”) is a trade name for a group of companies offering financial services that include both regulated and un-regulated affiliates. Investment advisory services are offered by Porter White Investment Advisors, Inc., an investment advisor registered with the SEC. SEC registration does not imply a certain level of skill or training.

[1] 401(k) plan overview | Internal Revenue Service

[2] Employee Retirement Income Security Act of 1974 (ERISA)

[3] Federal Bankruptcy Exemptions

[4] Hartley & Rauh (Stanford, 2022); PAP_IRA_20221231.pdf

[5] Vanguard Research (2025, empirical study)